757 Million Antennas: New Study Reveals Growth and Consolidation in the Cellular IoT Antenna Market

The global cellular IoT antenna market is growing strongly – yet a wave of acquisitions is reshaping the vendor landscape at the same time, and new technologies are confronting developers with changing design requirements.

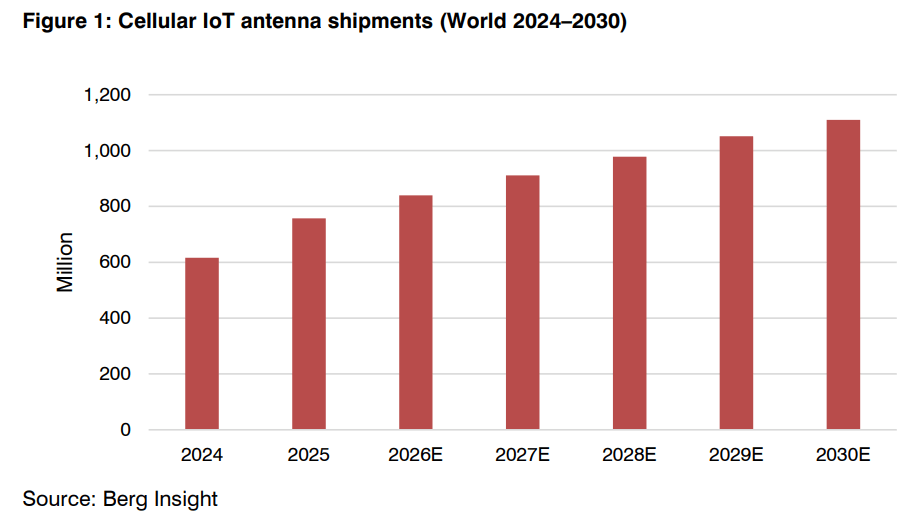

- Berg Insight estimates worldwide shipments of cellular IoT antennas – that is, antennas built into connected end devices such as trackers, vehicles or industrial sensors – at 757 million units in 2025, up 23 percent year-on-year, with growth forecast to continue at a CAGR of 7.9 percent to reach 1.1 billion units by 2030.

- Despite consolidation through acquisitions, the market remains fragmented: vendors range from large electronics manufacturers to specialists focused on individual form factors or vertical markets.

- In the internal antenna segment, software tools for antenna selection and design are gaining ground, while in the automotive segment, integrated antenna-TCU designs are challenging the classic shark fin form factor.

Last week, market research firm Berg Insight published the second edition of its report “The Global Cellular IoT Antenna Market”. The study is based on interviews with 20 industry executives and includes profiles of 32 antenna vendors.

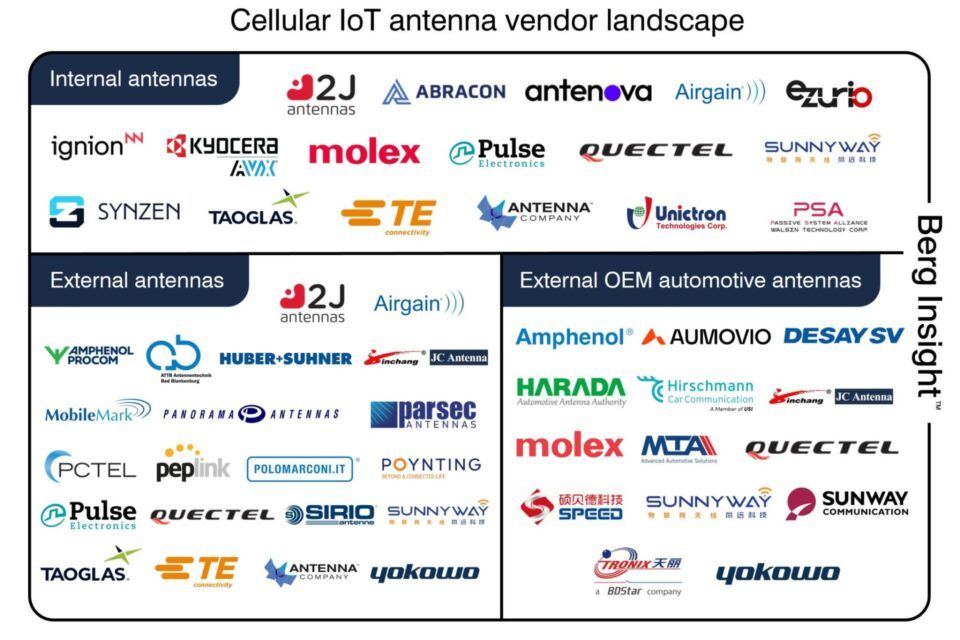

Three Segments, Little Overlap

Berg Insight divides the market into internal antennas, external antennas and external OEM automotive antennas. Internal antennas – antenna elements mounted directly on or within a device’s circuit board – dominate in terms of volume. External antennas serve more demanding use cases in industry, transport and critical infrastructure. According to the study, the vendor landscapes across the three segments show little overlap.

Internal Antennas: Off-the-Shelf Products and Software Tools on the Rise

In the internal antenna segment, most major vendors have increasingly shifted toward off-the-shelf products in recent years, moving away from resource-intensive custom antenna development. This approach enables more scalable and efficient growth. A growing trend alongside this is the introduction of software tools for antenna selection and design. Key vendors identified in the study include Taoglas, TE Connectivity, Sunnyway Technology, Kyocera AVX, Pulse Electronics, discoverIE (operating through 2J Antennas and Antenova), Quectel and Ignion.

M&A Shapes the Competitive Landscape

Several of the largest market players have built their positions through targeted acquisitions. Amphenol is today represented in the external antenna segment through Amphenol Procom and PCTEL; discoverIE brings together two specialised brands – 2J Antennas and Antenova – under one roof. Despite this consolidation, the overall market remains fragmented according to Berg Insight, driven by the breadth and diversity of end markets and form factors served.

Automotive: The Shark Fin Under Pressure

In the OEM automotive segment, most vehicles with embedded cellular connectivity continue to ship with roof-mounted combination antennas in the shark fin form factor. However, integrated antenna-TCU designs – solutions that combine the antenna and telematics control unit (the on-board module managing cellular connectivity and vehicle data) into a single unit – are increasingly gaining traction. Key vendors in this segment include Yokowo, Harada, Aumovio and Hirschmann Car Communication.

User Review

( votes)You may also like